Table of Contents

If you judged 2025 travel by the headlines alone, you’d think the industry was navigating a patch of turbulence. Government shutdown! Surprise ancillary fee changes! Budget airline bankruptcy! Viral stories about seat pricing, AI pricing, Real IDs finally landing, and a few harrowing headlines that didn't exactly inspire wanderlust.

Despite these noisy headlines, travel in 2025 was actually a little boring on the surface. Airfare yo-yo’d but stayed historically cheap. And travelers, by the looks of TSA numbers, chilled out. For the first time in years, we saw several months where fewer people flew than the year before—a sign that the post-pandemic frenzy has finally cooled.

But zoom in a little, and the picture actually does get more interesting. Mistake fares hit record-breaking levels. Summer prices looked delightfully pre-pandemic, and available last-minute to boot. Airlines reshuffled where they invested their resources, giving hungry travelers cushier seats and a taste of the tomato-girl lifestyle. Travelers went back to the drawing board, rethinking what a "good trip" means.

That's the backdrop for 2026. A year not of more trips, but of one big one. A year where trends can tank your hotel budget but can also save you 40% on airfare. A year where premium flyers enter a golden age, while deal hunters have to get a bit scrappier. A year where points are melting like ice cubes, not aging like a fine wine.

Travel isn’t in overdrive anymore. It’s in refocus mode.

Welcome to the Going 2026 State of Travel & Flight Deals. Boring on the surface. Fascinating underneath. And full of opportunities for the travelers who know where to look.

Chapter 1: The year of “one big trip”

Key takeaway: In 2026, travel isn’t about doing more. It’s about choosing well. As most travelers settle into a steady rhythm of fewer, more deliberate trips, the “one big trip” mindset anchors the year. And for Gen Z and solo travelers, that anchor digs deeper.

After years of post-pandemic overdrive, travelers are finally downshifting. They’re still traveling, just not traveling more. In 2025, nearly 39% of travelers said they took roughly the number of trips they expected. The frenzy has faded. The rhythm is returning.

But not everyone is slowing down. Almost half of Gen Z (48%) ended up taking more trips than planned, despite tighter budgets, busier schedules, higher airfare, and an unprecedented rise in safety concerns. For 2024 travel, 1.9% of average travelers said political and safety concerns were their biggest obstacle to travel. For 2026, 15.2% of average travelers anticipate it will be their biggest obstacle, now making it one of the top three barriers to travel.

And yet, they still go. Gen Z and solo travelers, who indicate they’re not planning to let up to the same degree, have more opportunities to make their trips count. But for the average traveler, the idea of “one big trip” has become both a constraint and an invitation. It’s forcing travelers to choose their trips more deliberately than they have in a long time—because a single trip holds the weight and wonder of an entire year.

So how will they make that “one big trip” count?

1a. Time to refocus

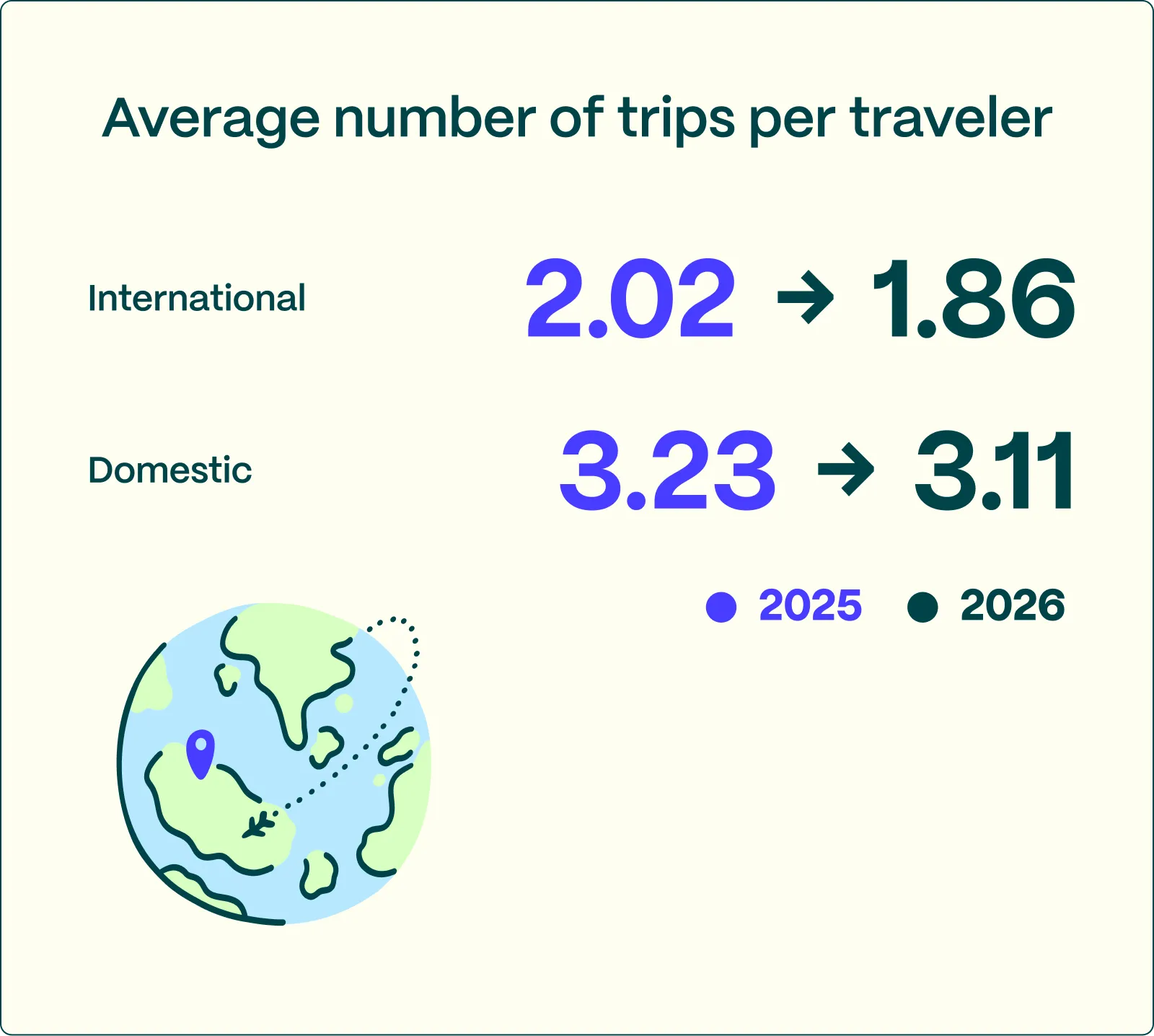

For most travelers, 2026 marks a shift toward fewer trips, both domestically and internationally. Planned international trips have dipped below the two-trip mark for the first time since 2023, meaning the majority of travelers are heading into the new year with a “one big trip” mindset.

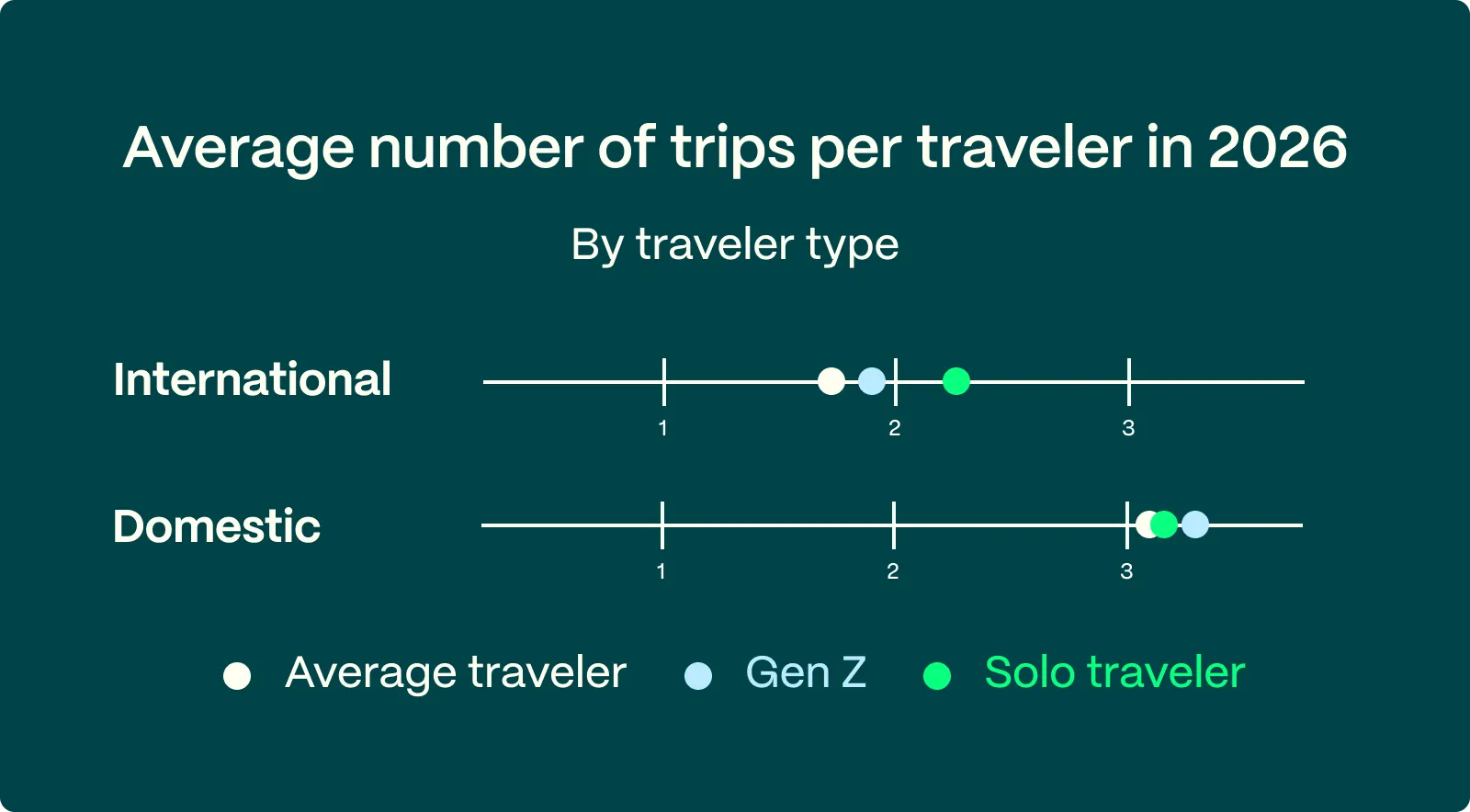

Gen Z and solo travelers aren’t letting up to the same degree. Both groups are intending to take more trips in 2026 than the average traveler, both domestically and internationally.

The sentiment behind travelers’ trips is also settling. For the average traveler, consistency is queen. They’re locking into a familiar rhythm: a couple of domestic flights, that one big, international trip, typically to places they already know and love—Europe, California, Florida, the hits. It’s comfortable, it’s reliable.

For Gen Z, travel is more than a respite. It's about exploring wider, deeper, and with more intention. They traveled more in 2025 than the average person, and they’re planning to again in 2026, despite higher financial and time pressures. While they have a lot more barriers, they’re putting their time and money toward the thing that matters to them: travel.

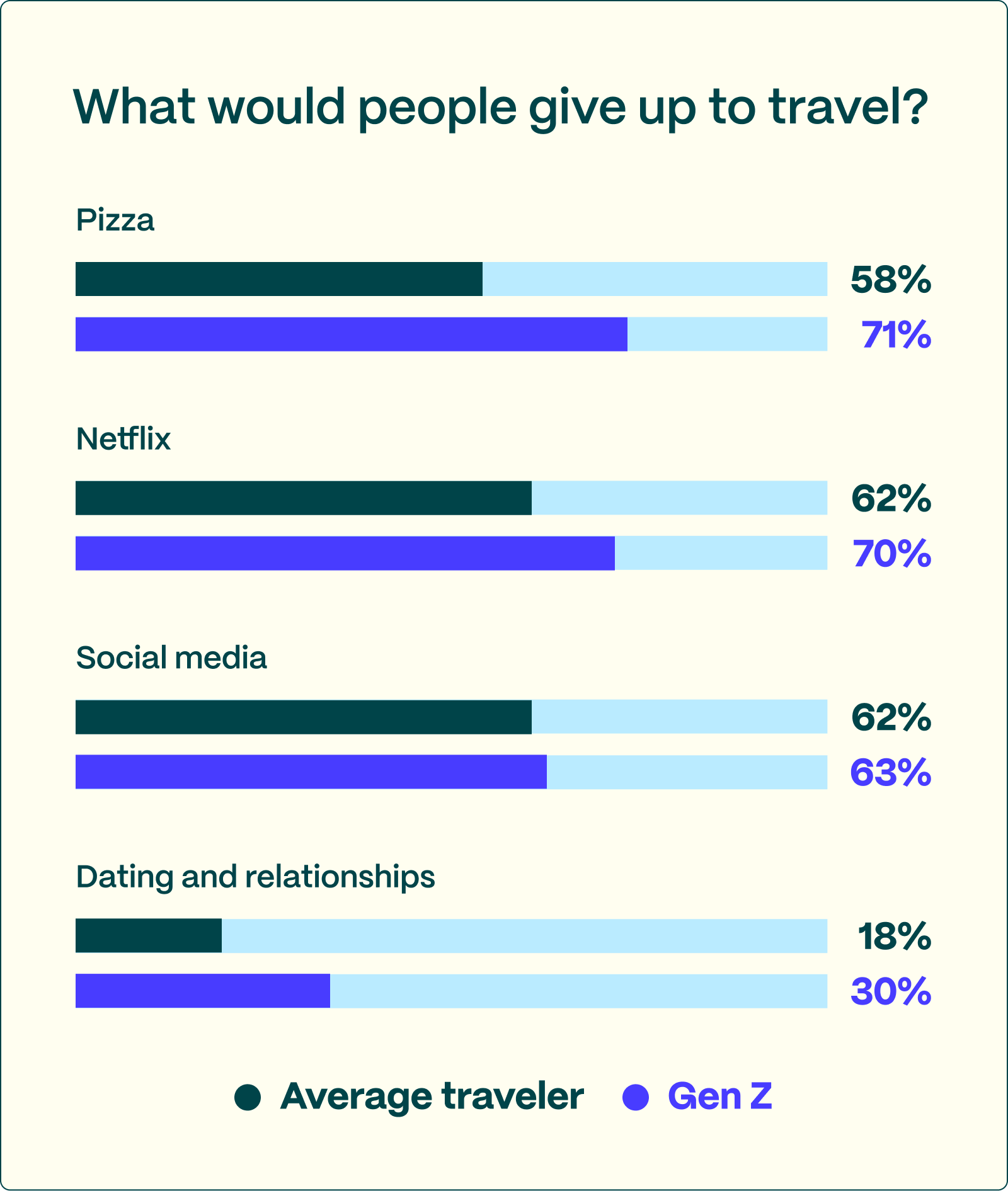

Compared to the average traveler, a lot more Gen Z travelers said they’d give things up in order to travel. Things like pizza, Netflix, social media, and even dating: For Gen Z, it’s no question. Travel is part of their identity, and they’re not willing to sacrifice it.

However, there are some things Gen Z may need to sacrifice, like the penthouse suite. While Gen Z is planning to venture farther and dig deeper (more on that below), they intend to spend a bit less in 2026 than they did in 2025. 23% of Gen Z plans to spend less on trips in 2026 versus 17% of average travelers.

And for Gen Z travelers who are planning to spend more, it’s because they’re taking longer trips to more diverse destinations. The average traveler’s reasons for spending more are less due to taking longer trips and more dependent on inflation pressures and intent to travel more luxuriously.

While solo travelers’ spending patterns aren’t vastly different from average travelers’, they, like Gen Z, intend to spend more because they’ll travel more and farther.

For most travelers in 2026, travel is a return to routine—but an intentional routine. Some will head back to the places that feel like home. Others will chase the trips that change them. So where is everyone heading?

1b. Where’s everyone going?

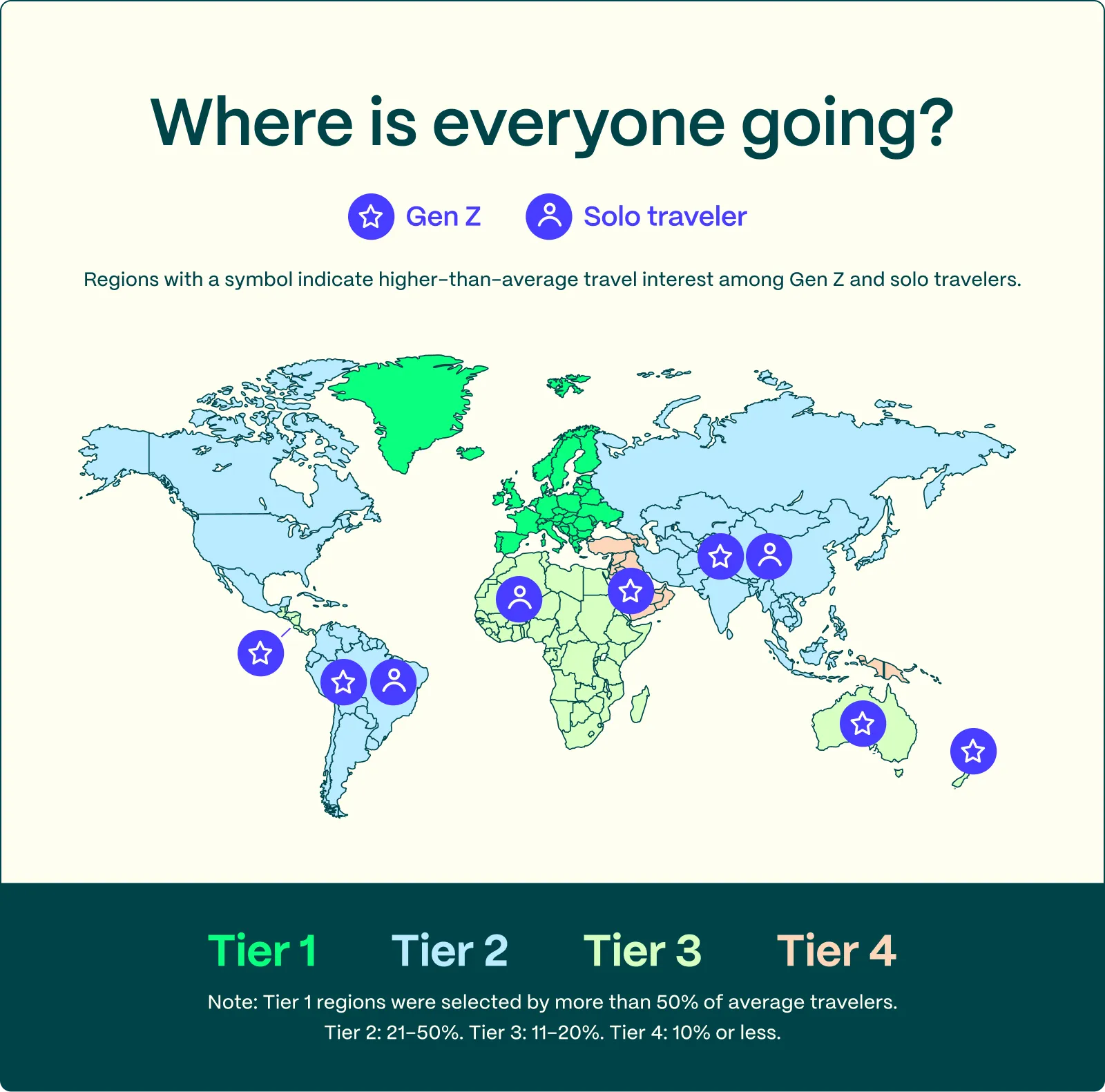

International: Europe cools, Asia heats up, Gen Z and solo travelers go farther

Europe still leads overall travel interest (74%), but enthusiasm is cooling—down five points from last year and the steepest decline of any region. The post-pandemic rush to “finally do Europe” is settling into something more selective. Rising costs and a strong euro may be pushing some travelers to diversify.

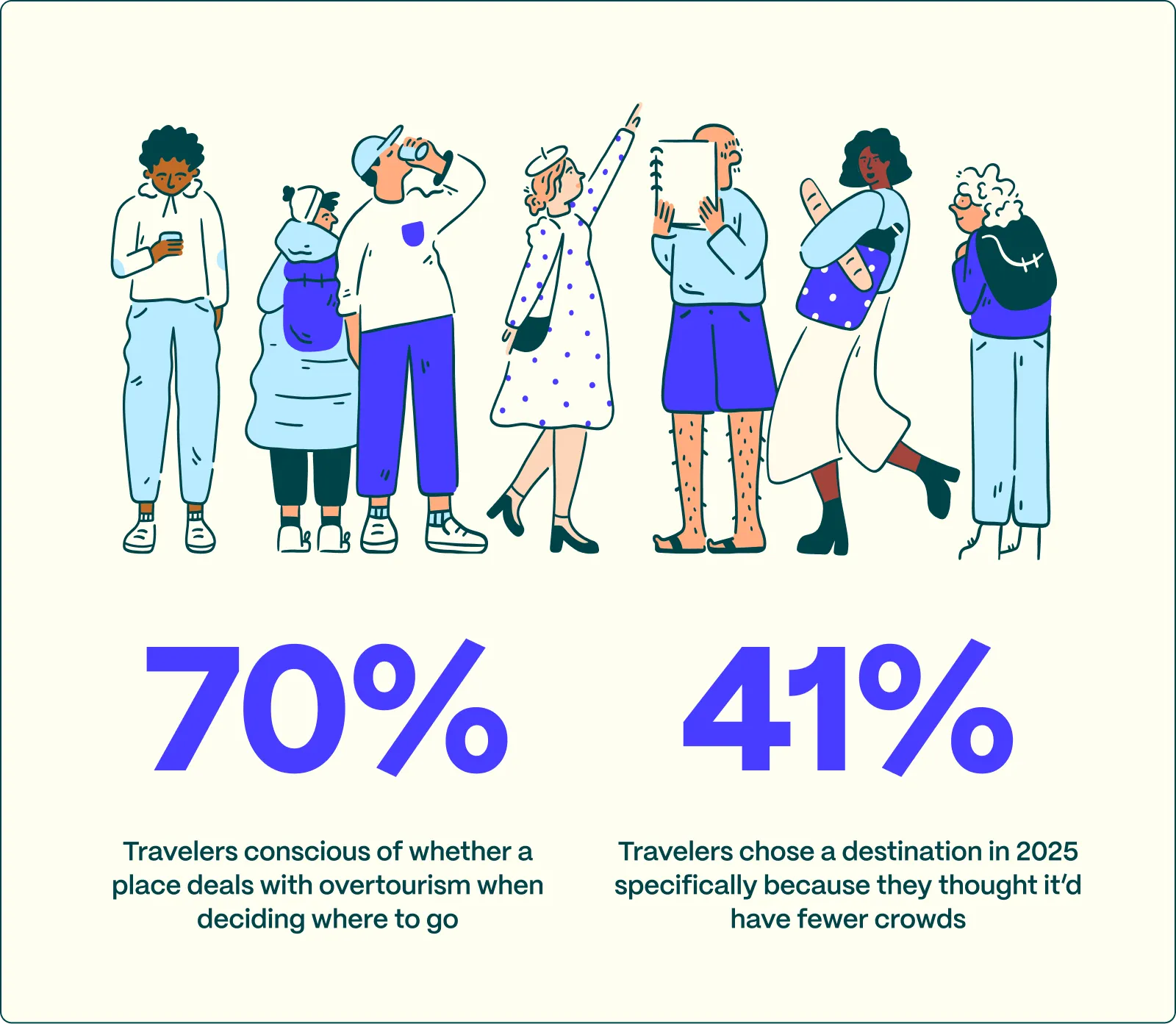

Big crowds are proving to be a deterrent, as well. More than 70% of respondents said that, when choosing a destination, they are conscious of whether it deals with overtourism. In 2025, 41% of respondents said they chose a destination specifically because they thought it’d have fewer crowds.

Asia, on the other hand, is holding—and growing. Going search data also shows that interest is expanding beyond Japan to Thailand, South Korea, the Philippines, and Taiwan, with key European cities falling in the ranks.

Among Gen Z, the shift is pronounced:

- 47% express interest in Asia (vs. 33% average travelers)

- Higher-than-average interest in South America, Central America, Australia/New Zealand, and the Middle East

Rather than sun-and-resort vacations, they’re focusing on culture-forward, food-forward, experience-first itineraries—often longer, slower, and more immersive.

We’re also seeing shifts among solo travelers, with above-average interest in Asia, South America, and Africa, reflecting a desire for independence and discovery beyond the norm.

Looking for experience-first inspiration? Check out these trips that we think will be worth the flight in 2026:

- Feast under the northern lights in the Canadian tundra

- See king penguins in a Patagonia nature reserve

- Bike from Seoul to Busan on the 4 Rivers Path

- Listen to fado in a Lisbon tavern

- Hop over to Kangaroo Island from Adelaide

- Hike the 96-mile West Highland Way in Scotland

Domestic: Not disappearing, but diversifying

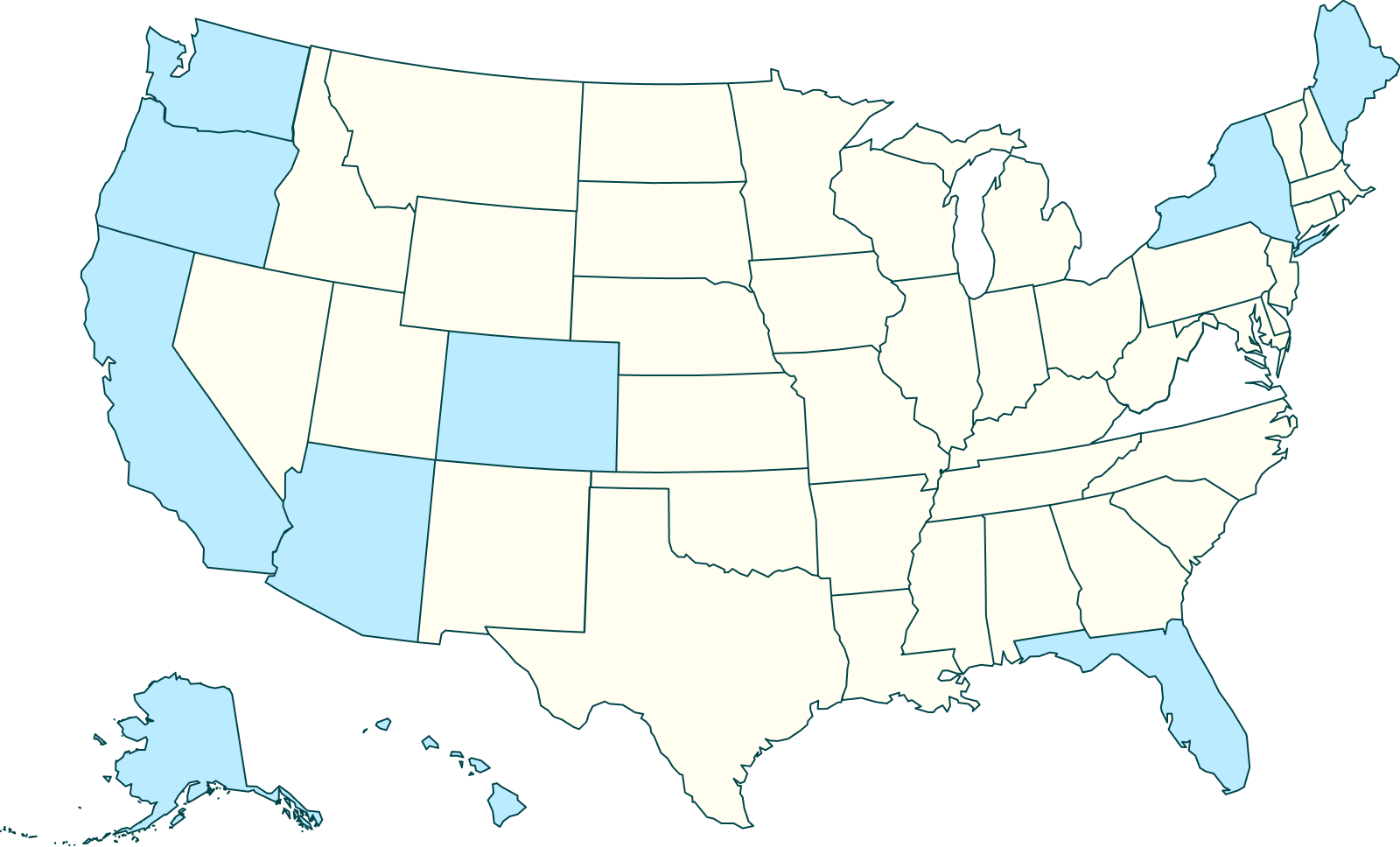

Domestic travel isn’t declining so much as stabilizing. The big-name states (California, New York, Florida) still draw solid interest, but more travelers—especially those taking “one big trip” domestically—want places that feel meaningful, novel, or restorative.

The result is a quiet rise in demand for states such as Alaska and Maine, and a decrease in demand for states like Hawaii, where visitors may have visited in recent years and are ready to branch out from.

Trip types: Cities dominate, nature regenerates, beaches steady

For the average traveler, cities remain the powerhouse, buoyed by food, culture, and a craving for stimulation after years of caution. At the same time, small towns and countryside destinations see a modest uptick, reflecting a continued interest in slow travel.

For Gen Z, the split is even more pronounced:

- 88% plan to visit a city in 2026: higher than the already-strong average population

- Nature is non-negotiable: 62% plan to visit national parks or forests—far outpacing other age groups

Gen Z, more than any other group, seeks a balance: the energy and creativity of cities and the grounding clarity of nature. Their “one big trip” often includes both.

1c. Traveling with purpose—and deals

The deal isn’t dead, but other influences are creeping in. Even for Going members, overall reliance on flight deals dropped about ten points year-over-year.

However, Gen Z breaks that rule: 6 in 10 still plan their trips around finding a deal, indicating they’re both value-driven and discovery-driven.

In 2026, travel is increasingly:

- To feel something (connection, creativity)

- To see someone (friends, communities)

- To experience something (culture, events)

The average traveler’s top reason for traveling is to visit family and friends (55%). But for Gen Z, arts and culture is now the #1 motivator, with outdoors the top motivator in 2025. Meanwhile, traveling for history falls to the bottom (42%).

Attractions and events will also see an uptick in 2026 (46% vs. 43% in 2025), with more than 1 in 3 people traveling for a cultural event or festival. Music, food, and sports will also have travelers hopping on a plane.

Chapter 2: Where to go in 2026 if you love cheap flights

Our list for 2026 starts with one simple question: Where will it actually be cheaper and easier to fly in 2026?

We built this list around the real deals, not wishful thinking. Every destination earned its spot because something shifted in the skies: new routes, expanded long-haul service, competitive low-cost lift, airport upgrades, or visa changes that unlock better prices and smoother connections.

Will your big trip in 2026 be a break from the Mediterranean crowds to catch an art show in a Maltese medieval fortress, or feast on chewy focaccia at a family-run shop in Puglia? A cross-country tour to celebrate the Mother Road’s centennial? A night of lantern-lit snacking in a Taiwanese night market? A long weekend wandering Cartagena’s pastel balconies? A sunrise stroll through Marrakesh’s spice-scented souks?

If one of these destinations is on your list, the skies are making it easier and cheaper to get there. And if they’re not on your list…maybe they should be.

Chapter 3: Going deal report: Price thresholds for top destinations in 2026

2025? Boring. Travel frenzy? Faded. Fares? Still golden.

If you’ve paid attention to fare trends throughout 2025, you know it requires as much zoom lens to analyze as the rest of the year. The stark drop in average fare price in the first half, plateau in June, and subsequent spike heading into the second half felt like anything but solid ground. But this time, let’s zoom out.

Fares may fluctuate modestly month to month, but airfare today is dramatically cheaper than it was 10, 15, 20 years ago. In fact, adjusted for inflation, June 2025 was the second-cheapest month for airfare on record. Yes, ever. And barring major shocks, 2026 is poised to be just as fruitful when it comes to flight deals.

To this, we’ll address everyone’s burning question: Yes, we are still in the Golden Age of Cheap Flights.

Chapter 4: Viral vacations mean cheaper flights—but more expensive trips

Key takeaway: Travel trends can save you tons on flights, but they can cost you a bunch more once you land. In 2026, the smartest travelers will know what’s trending—then look just beyond it.

Travel has always had its hotspots, but in 2026, “hot” has become algorithmic. A TV show, a viral itinerary, or an influencer’s highlight reel can rocket a destination into the stratosphere. And the ripple effects aren’t subtle: more flights, fuller planes, pricier hotels, crowded attractions, and a collective FOMO that drives people to book trips they may not have otherwise considered.

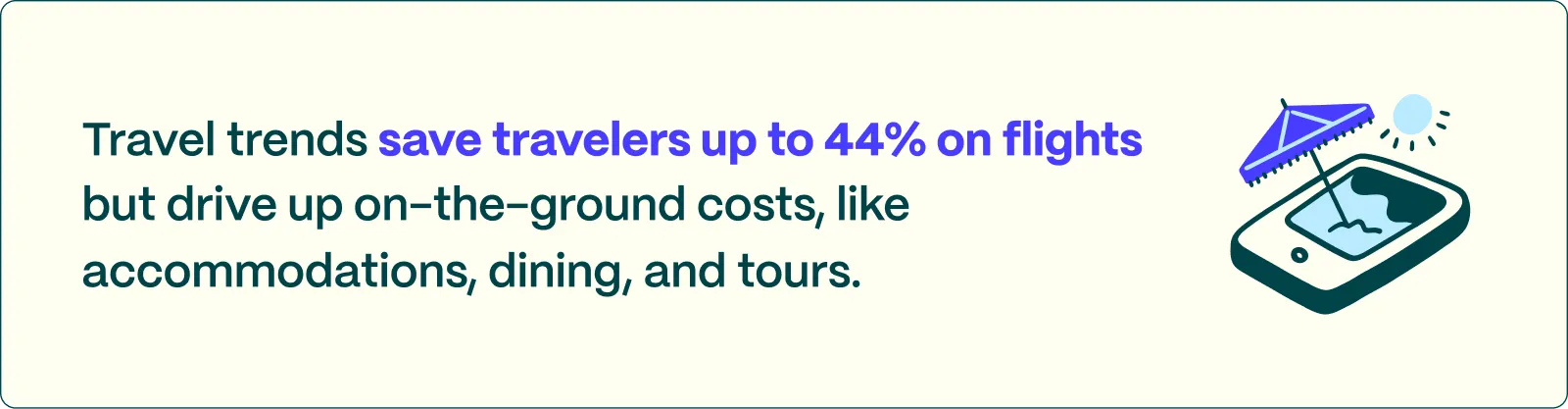

Basically, “travel trends” are now trending. It’s travel trend-ception. It’s the trendification of travel. And it can save travelers up to 44% on flights—but it’s costing them in plenty of other ways.

4a. The upside: Trend-driven demand drags airfare down

You saw a place on TV? You heard about the next big “it” destination on Instagram? Airlines are paying attention. They pour capacity into trending destinations, add new routes, and increase frequency, all of which can push airfare lower and make once-niche locations more accessible.

We’ve seen “trendification” slash fares by double digits:

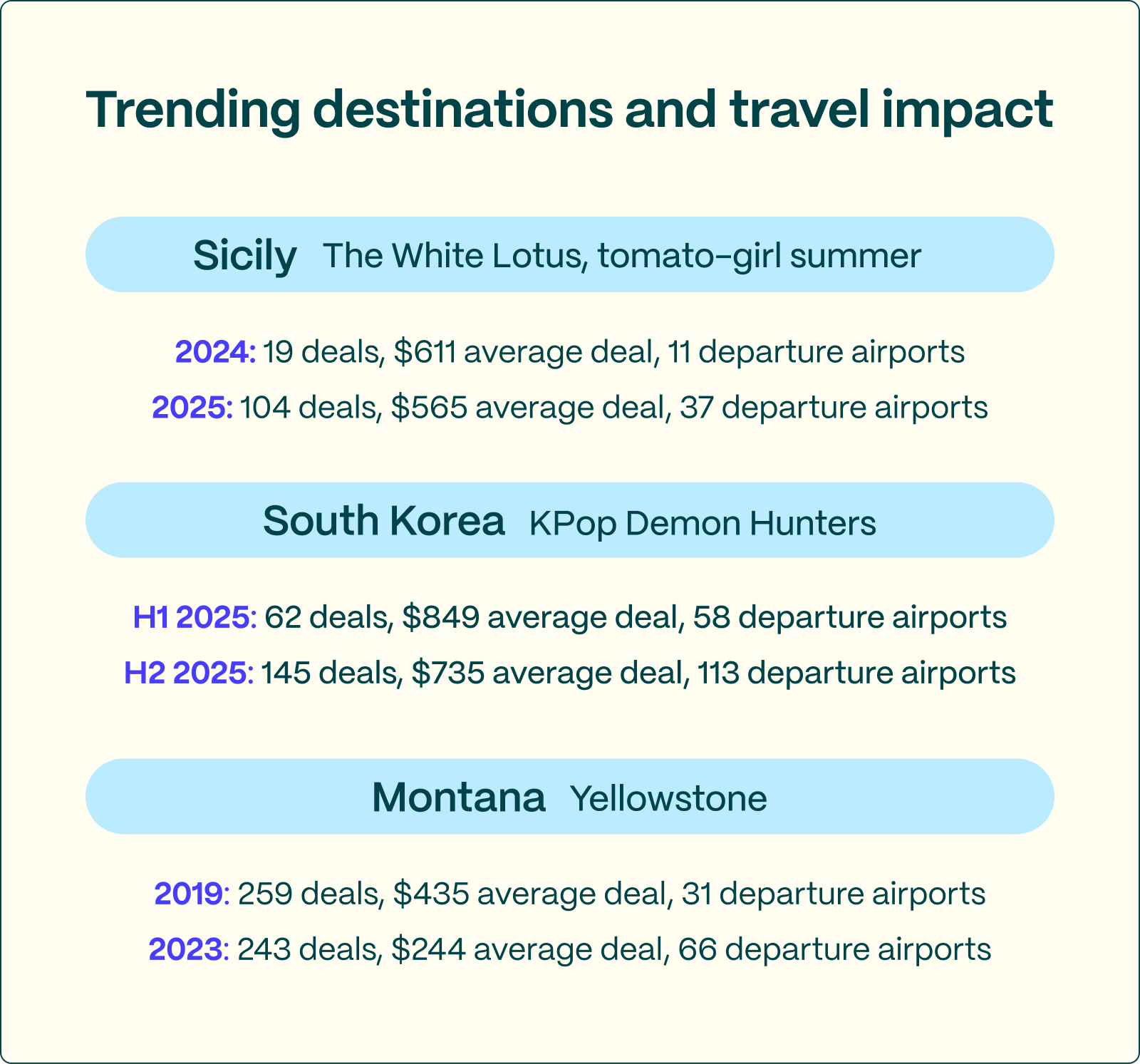

- Sicily deal volume increased 5x and average price decreased 7% after “The White Lotus: Season 2” aired (and probably a little thanks to the tomato-girl summer trend)

- South Korea deal volume increased 2x and average price decreased 13% after “KPop Demon Hunters” aired

- Montana deal volume stayed relatively stagnant but average price decreased 44% after “Yellowstone” aired and the subsequent “cowboy culture” took hold

Trend cycles can be chaotic, but they also democratize access to the destinations. Suddenly, places that felt aspirational start showing up in inboxes $100s less than they were last year.

4b. The downside: Everything else gets more expensive

Cheaper flights don’t equal cheaper vacations. Hyperfixation on the same handful of destinations spikes demand on the ground, as well—hotels, restaurants, tours, car rentals, even museum reservations. The result: What you save on airfare, you can easily lose the moment you step off the plane.

Look at what happened after “The White Lotus: Season 2” aired: Airlines ramped up service to Sicily and airfare dropped, but hotel prices soared and local infrastructure struggled under the surge. Same story in Tokyo, Seoul, Dubrovnik, Iceland, and Jackson Hole. The more social currency a destination has, the more travelers pay to “keep up.”

4c. Straight from the horse’s (or influencer’s) mouth

Between 2025 and 2026, the way that people discovered their next destination shifted strongly toward trusted sources, be them IRL or on social media.

- Friends and family recs rose to the top spot, now the #1 travel influencer: Real experiences from real people carry more weight than ever.

- Social media influence rose 3 percentage points overall, now 25%: But for Gen Z, it’s a tidal wave. Nearly half of all Gen Z travelers say their 2026 destination interest was dictated by what they saw on social media.

- AI entered the chat: 6% of travelers say an AI tool told them where to go in 2026, adding algorithmic momentum to already-trending destinations.

This can come at a cost. When everyone sees the same 20 destinations on Instagram, those 20 destinations get crowded fast, while hundreds of equally incredible, far cheaper destinations go unnoticed.

4d. A game of Keeping up with the Joneses

In the words of Ariana Grande: “I see it, I like it, I want it, I got it.”

Travelers see a place on Instagram, they like what they see, they want to go there, they book the flight—even if it costs 44% more than it did last year (or even in the off-season).

Influenced by social media, travelers are now willing to pay top dollar to keep up with the Joneses (or the TikTokers). The pull is emotional and fast, often overriding budget, timing, and logic.

4e. The Going take

Buck the trends, and save big. Paris will always be there. Sicily and Seoul, too.

Visit in the shoulder season. Visit in the winter. Visit when it’s not going viral. Or, skip the trends entirely and follow the deals that you’d least expect.

Barcelona might be at capacity, but Basque Country is wide open. Tokyo is booked up, but Taipei has better restaurant availability and cheaper hotels. Sicily is having a moment, but Malta is having a year.

Trendification is a double-edged sword. It can unlock cheaper flights, more routes, and unexpected opportunities, but it can also funnel travelers into the same places at the same time, driving up costs and crowding out authentic experiences.

For 2026, the smartest strategy is simple: Know the trend—but don’t be ruled by it. Follow the deals, embrace the off-season, and remember the golden rule. The destination isn’t going anywhere.

Chapter 5: It’s boom time for premium travelers

Key takeaway: Better premium seats, more long-haul direct routes, enhanced lounges—it’s never been a better time to be a bougie traveler. While opportunities for cheap-flight lovers are dwindling, they’re certainly not gone.

For years, air travel has been defined by a tug-of-war between cheap fares and fierce competition. But heading into 2026, the picture looks different. The industry is experiencing a full-on K-shaped divergence, where the upper arm of the “K” (premium cabins, brand-loyal flyers, and luxury-leaning travelers) is soaring, while the lower arm (full of cheap-flight-loving travelers) is dragging.

Why? Demand has shifted, and airlines have followed.

If you’re a traveler of the Finer Things Club, this is your era. And if you’re bargain-minded, it’s not all bad—but let’s just say the glory days may be slightly harder to grasp.

5a. Premium upgrades for some, shrinking options for others

Premium travel has never been stronger. Legacy carriers, like Delta and United, are operating as confidently as ever, pouring resources into what is essentially a golden age of upgraded seats, new long-haul direct routes, better onboard service, and premium cabin experiences. After years of cuts and compromises across the industry, these airlines aren’t just recovering, they’re thriving.

At the same time, budget airlines—once industry disruptors—are struggling to keep up. Costs are up, margins are thin, mergers are impending, and several low-cost carriers are pivoting toward quasi-premium models, with roomier seats, loyalty perks, and upgraded onboard services, to stay afloat. In fact, they’re looking suspiciously legacy-like.

This shift means one thing for the cheap-flight lover: While, in the grand scheme, flights are cheaper than they’ve ever been, the real gems can take a bit more digging to find. The cutthroat price wars of the 2010s are gone. Airlines aren’t battling each other on cost the way they once did, thanks to higher demand for premium seats, broader adoption of airline credit cards, and travelers who increasingly prioritize comfort and brand loyalty.

5b. A premium boom fueled by travelers’ behavior—and their wallets

Going’s 2026 State of Travel & Flight Deals confirms the luxury momentum. Although most travelers aren’t planning more trips next year, many are planning to spend more, and not because they’re traveling more often. They’re spending more because:

- inflation is creeping in

- they’re opting for more intentional trips, and they’re willing to spend more to make those trips count

- major milestone events (like the World Cup, concerts, solar eclipse trips, weddings, big birthdays, and more) demand higher budgets

Their top splurges:

- 71%: better accommodations

- 59%: premium cabin seating

- 52%: upgraded destination experiences (e.g., VIP events, tours, special access)

Premium economy—the gateway to nicer travel—is the fastest-growing cabin choice, jumping from 16% to 20% of travelers this year. On the flip side, fewer people are willing to book budget airlines (44% vs. 50% in 2025).

So while travelers aren’t necessarily spending more often, when they do spend, they want to do it right. Comfort is rising as a deciding factor, up from 19% to 21% year-over-year. Price is still important, but comfort is catching up.

5c. Why 2026 is a golden age for bougie travelers

Over the post-pandemic years, airlines have invested in premium cabins and the elite-status experience, as margins for selling these seats are higher than in economy. Add in the prevalence of airline credit cards, which boost loyalty while reducing price sensitivity, and the result is an industry environment with far less pressure to compete on cheap fares.

Pre-pandemic, price was the primary deciding factor for the average traveler. Now it’s:

- loyalty program benefits

- brand loyalty

- reliability

And for bougie travelers, their dollars are stretching further than ever. The premium experience—things like cabin products, elevated airport lounges, and more direct routes—is the best it’s been in decades. It’s a boom time for travelers of the Finer Things Club.

These are sample deals that we’ve recently sent for premium cabins with availability in 2026:

- Seattle to Paris for $935 roundtrip in premium economy

- NYC to Marrakesh for $994 roundtrip in premium economy

- Houston to Tokyo for $1,531 roundtrip in premium economy

- Chicago to Milan for $2,964 roundtrip in business class over Christmas

- Miami to Cairo for $2,258 roundtrip in business class (lowest since 2021)

5d. The silver lining for cheap-flight lovers

Even though the premium world is thriving, economy travelers still have options. Cheap flights are certainly out there—if not, we wouldn’t exist—and a bit of luxury may be more attainable than most assume.

One of the few remaining “value hacks” in the era of shrinking budget options is, surprisingly, the airline-branded credit card. Yes, fees are up. Yes, programs devalue. But for 1–2 checked bags, early boarding, and better seat selection—especially if you fly more than a couple times per year—the math works out.

The fact of the matter: With so many people now holding airline cards, 90% of your flight will board ahead of you. Unfortunately for cheap-flight lovers in 2026, it’s a game of keeping up with the Joneses if you want even a taste of luxury.

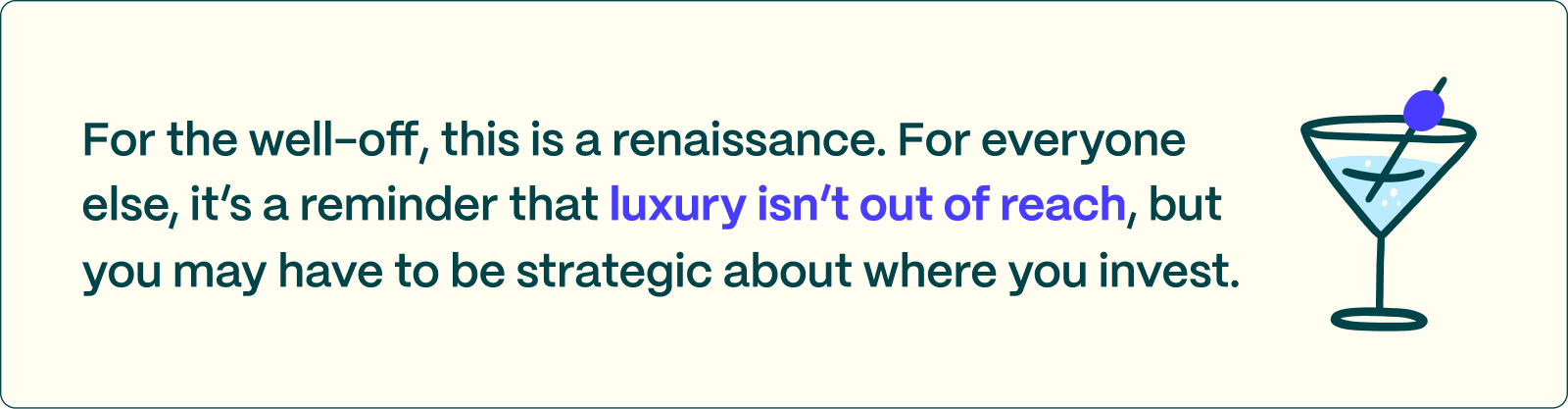

While luxury is no longer out of reach, you may have to be strategic about where you invest.

Chapter 6: 3 things even points and miles pros might not know heading into 2026

Key takeaway: Don’t sit on your points in 2026—spend them.

Like a fine wine, points can elevate any trip, turning a long-haul flight into a lie-flat moment or a standard stay into something suite-r. But unlike fine wine, they don’t get better with age. Points devalue quietly—and apparently quickly. Award charts shift. Programs change the rules mid-game. The longer you wait, the more value you’re losing.

2026 is the year to use your points, not save them for “someday.” Here’s what points-savvy travelers need to know now.

6a. The value of points is slowly decreasing

Points don’t age well because loyalty programs keep changing the rules. And lately, those changes have tended to make your points less valuable, not more.

Notably, in 2025, Air France–KLM’s Flying Blue, Singapore Airlines’ KrisFlyer, and British Airways’ Avios raised award prices by 5–20% depending on the route and cabin. In some cases, additional cash surcharges on bookings have increased as well.

This is the new pattern:

- More miles required for the same routes you used to book

- Dynamic award pricing that surges when demand does

- “Saver”-level award seats that are harder to find

- Hotels using seasonality and market data to nudge award costs upward

Whereas loyalty programs may have once been relatively fixed, they now move more fluidly with the market.

What does this mean? The value of your points today is almost always higher than the value of your points six months from now. Waiting for the “perfect redemption” is no longer strategic—it’s risky. The longer you sit on your points, the more likely you’ll wake up to another quiet devaluation.

6b. Business class to Asia and Oceania is one of the best redemptions in 2026

Not because it’s flashy, but because the value per point is currently strongest on long-haul routes to Asia. Why?

- A dense network of airline partners means more opportunities

- Award space is returning as routes expand

- Cash prices remain high, widening the value gap

Economy flights to Australia and New Zealand are also seeing standout value windows, especially when booked with flexible partner programs.

Roundtrip points deals we’ve sent to Asia and Oceania for 2026 travel include:

- 37k–74k points to Seoul in economy from January–December 2026

- 49k–58k points to Tahiti in economy from January–September 2026

- 50k points to New Zealand in economy from January–March 2026

- 122k–146k to Taipei in business class from January–September 2026

So if you have been saving points for a “someday” long-haul, this may just be your sign to set your sights on Asia or Oceania.

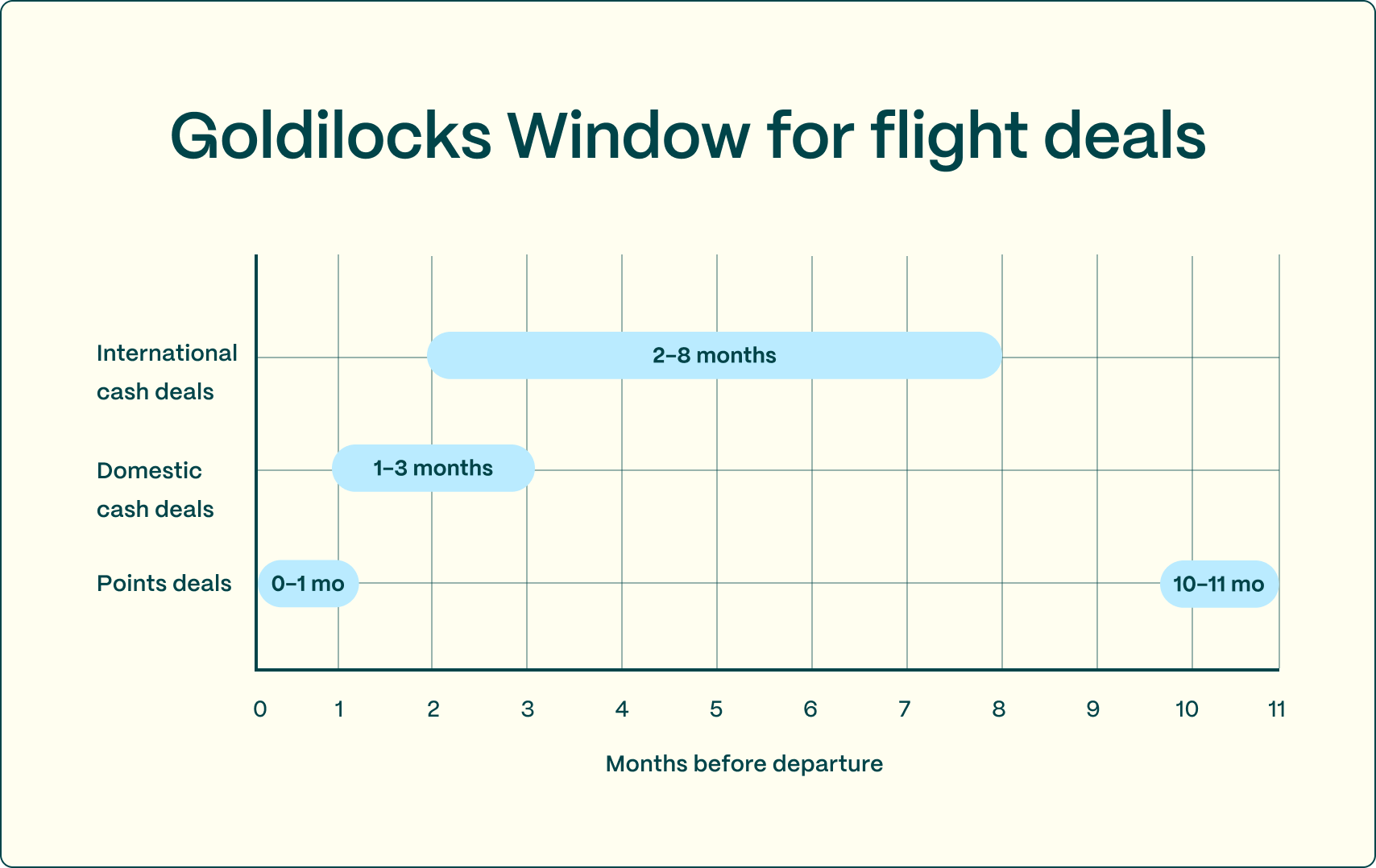

6c. The Goldilocks Window hits different for points

The “Goldilocks Window”: not too early, not too late, right in that sweet spot when you’re most likely to find a great fare. If you’re paying with cash, the window is 1–3 months ahead of departure for domestic and 2–8 months ahead for international (add a couple months if you’re traveling during a peak season, like summer, winter holidays, or Carnival in Rio).

Award travel, however, plays by its own rules. The curve looks almost inverted compared to cash prices.

When you’re using points and miles, availability tends to peak at two different times: when airlines release their schedules (about 10–11 months out), and then again in the final weeks before departure. In between, the period when cash deals are often at their cheapest, can actually be the worst time to find good redemptions.

Here’s the gist of why this happens: When schedules first open, airlines often release a handful of saver-level award seats per flight, particularly in business class. As demand takes shape, those cheaper award seats often disappear. Then, as departure approaches and airlines reconcile how many seats are likely to go unsold, they quietly release another wave of award seats.

Counterintuitive? Maybe. But pretty consistently that’s what happens: Award space often dries up during the months when cash fares are typically cheapest.

So if you’re trying to travel on points, it’s time to rethink the usual playbook. The Goldilocks Window for cash fares might still be golden, but for award travel, the sweetest spot can be much earlier or much later. Want the best shot at premium cabins, long-haul routes, or ultra-popular destinations? Look right when the schedule opens. Missed that window? Check again when your trip is getting close, much closer than you’d assume.

Cash has a Goldilocks Window. Points have bookends. Knowing the difference can be the key to unlocking the award seat everyone else swears doesn’t exist.

Methodology

This report draws on survey responses from 7,008 Going members, offering insights into traveler attitudes, behaviors, and planning patterns. Quantitative findings are supported by proprietary flight deal and search data collected from January 1, 2025, to November 20, 2025, unless otherwise specified. Where relevant, external industry benchmarks and secondary research sources were incorporated to contextualize trendlines and compare traveler sentiment against broader market indicators.

Last updated March 6, 2026